Why Profit Alone Does Not Keep a Business Alive: A Practical Cash Flow Guide for Small Businesses

Your business can earn strong profits and still may collapse. Why?

Because profit is an accounting number. Cash is operational survival.

Many small businesses do not fail because their products are bad or because customers disappear. They fail because cash does not arrive when obligations become due. Salaries, supplier payments, rent, taxes, loan installments, and utility bills all require immediate payment.

For small businesses like yours, cash is not just important — it is operational oxygen.

This guide explains why cash flow problems happen and what business owners can do to stay financially stable.

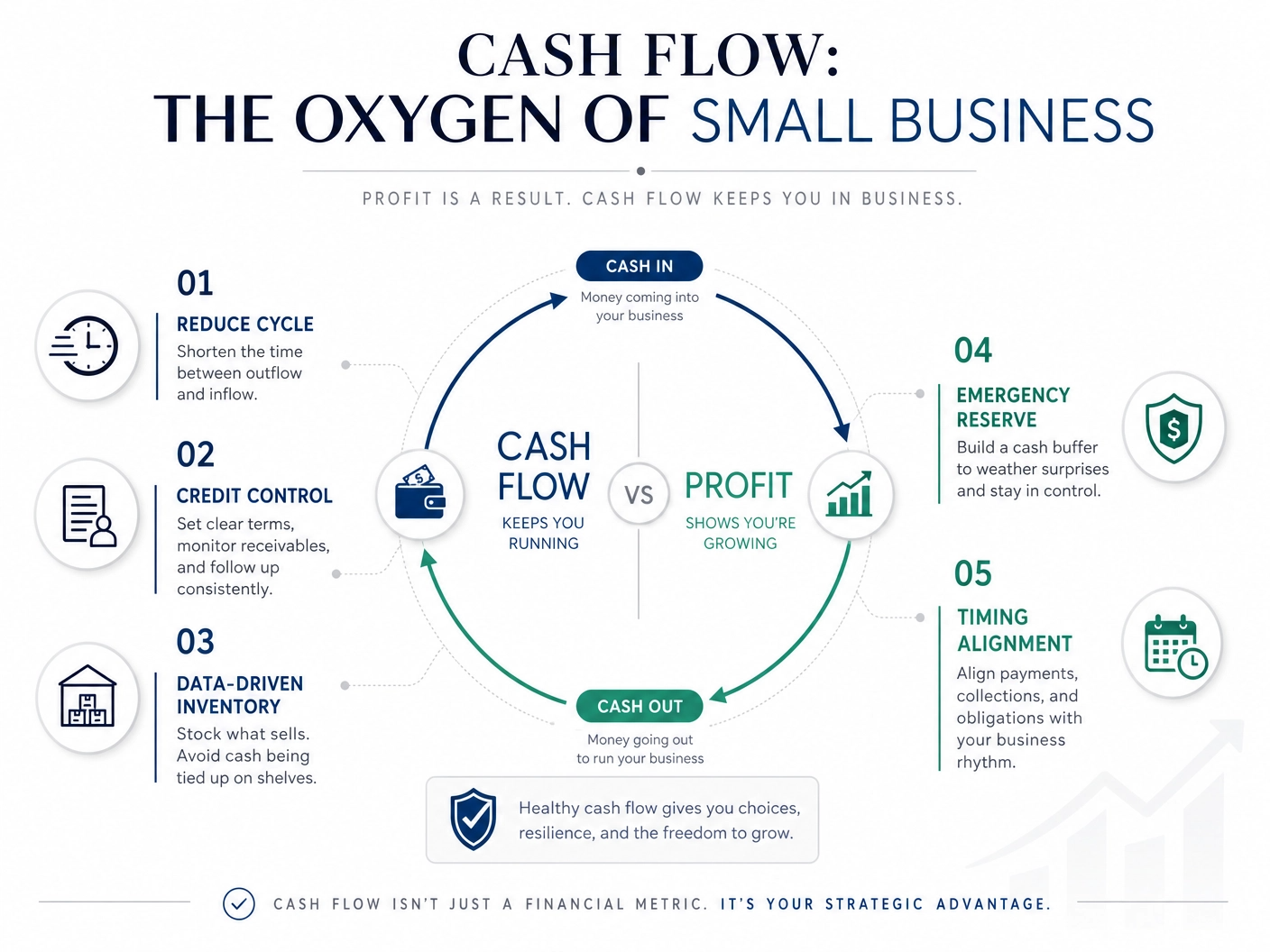

1. Profit Is an Accounting Result. Cash Is a Business Reality.

Profit measures performance over time.

Cash measures survival today.

Suppose your business completes a project worth Tk. 500,000 in January under a 60-day payment term. The income statement (profit & loss accounts) may show a healthy profit immediately. However, if the client pays you in March, your business still needs to fund salaries, rent, internet bills, transport, and supplier payments during January and February.

Your business may appear profitable on paper while struggling to pay daily expenses.

This is the core difference:

- Profit tells you whether your business model works.

- Cash flow tells you whether your business can continue operating.

Your business pays obligations with cash, not with receivables recorded in your accounting books.

2. Long Payment Terms Create Dangerous Working Capital Pressure on your Business

Many small businesses like yours accept delayed payment terms to attract or retain large clients. Net-30, Net-60, or even Net-90 arrangements are common in service industries, trading businesses, and corporate supply chains.

In practice, this means your small business finances the operation first:

- Pay staff salaries immediately

- Purchase materials upfront

- Logistics and operational costs continue monthly

- But customer cash arrives much later

This creates a working capital gap.

Without adequate reserves or financing support, you often respond by:

- delaying supplier payments,

- using expensive short-term borrowing,

- missing tax obligations,

- or using personal savings to sustain operations.

Over time, this weakens the financial stability of your business.

A growing business like yours with weak cash management can become more vulnerable than a smaller but cash-disciplined business.

3. Inventory Can Quietly Drain Cash

If your business is product-based, inventory is one of the biggest cash traps.

Every unsold product sitting in a warehouse or showroom or shop represents money that is no longer available for:

- marketing,

- payroll,

- debt repayment,

- or future opportunities.

The problem becomes worse when inventory is sold slowly.

Seasonal demand changes, forecasting mistakes, or declining customer interest can lock cash inside products for months. Meanwhile, the business continues paying:

- warehouse rent,

- storage costs,

- insurance,

- maintenance,

- and financing expenses.

Healthy inventory management means inventory must convert back into cash fast enough to support the next purchasing cycle.

Inventory should support liquidity — not destroy it.

4. Fast Growth Can Create Cash Flow Crises

Growth sounds positive, but unmanaged growth can damage your business.

Expansion usually requires spending before revenue arrives:

- hiring employees,

- increasing production,

- purchasing equipment,

- expanding inventory,

- opening branches,

- or increasing marketing expenses.

These investments consume cash immediately.

If sales collections are delayed or projected growth slows, your business faces pressure despite strong demand and a healthy order pipeline.

This is why many rapidly growing businesses experience financial stress.

Growth without cash planning creates instability.

Smart businesses scale only when their cash position, reserves, and financing structure can absorb temporary shocks.

5. Managing Without a Cash Forecast Is Risky

Many small business owners manage finances by checking their bank balance or cash in hand.

But a bank balance or cash in hand only shows the present moment. It does not show:

- upcoming supplier obligations,

- payroll commitments,

- tax deadlines,

- loan repayments,

- or delayed customer collections.

Professional finance teams use rolling cash flow forecasts to predict future liquidity positions.

One of the most practical tools is a 13-week cash flow forecast.

It tracks expected:

- customer inflows,

- operating expenses,

- payroll,

- taxes,

- debt payments,

- and major purchases.

The purpose is simple: identify cash shortages early enough to take corrective action.

Without forecasting, management reacts under pressure.

With forecasting, management plans ahead.

Five Practical Ways to Strengthen Cash Flow

1. Reduce the Cash Conversion Cycle

Your business should aim to collect cash faster and delay unnecessary outflows responsibly.

Practical actions include:

- requesting advance deposits,

- invoicing immediately after delivery,

- offering small early-payment incentives,

- and simplifying payment methods through digital payment systems.

The faster cash returns to your business, the healthier operations become.

2. Strengthen Customer Credit Control

Not every sale is a good sale.

Before extending credit:

- verify customer reliability,

- define payment terms clearly,

- follow up consistently,

- and enforce consequences for late payment.

For repeat late payers, you should consider:

- partial advance payment,

- shorter payment cycles,

- or suspension of further service until outstanding balances are settled.

Strong collection discipline protects your liquidity.

3. Manage Inventory Using Data, Not Assumptions

You should take inventory decisions based on actual sales movement and turnover patterns.

You should:

- monitor fast-moving and slow-moving products,

- set reorder levels carefully,

- reduce dead stock quickly,

- and avoid over-purchasing based on optimism alone.

Recovering partial cash from excess inventory today is often better than waiting indefinitely for a full-price sale that may never happen.

4. Build an Emergency Cash Reserve

Every business should maintain a liquidity buffer. You should have a practical target for maintaining reserves equal to:

- 3 to 6 months of fixed operating expenses.

This reserve should cover:

- payroll,

- rent,

- utilities,

- essential software,

- and core operating costs.

The reserve is not for expansion or unnecessary spending.

It exists to protect your business continuity during periods of delayed collections or economic uncertainty.

5. Align Cash Inflows and Outflows

Your business must carefully match the timing of incoming and outgoing cash.

Examples include:

- negotiating supplier terms similar to customer collection terms,

- staggering large expenditures,

- avoiding excessive fixed commitments,

- and using financing strategically for timing gaps rather than operational losses.

Good cash timing reduces financial stress significantly.

Final Thoughts

Profit is important. It proves that your business model can generate value.

But profit alone does not guarantee business survival.

A business with temporary accounting losses may still survive if it maintains healthy cash reserves. A profitable business without liquidity may fail unexpectedly.

This is why disciplined cash flow management matters.

Business owners like you should:

- forecast cash weekly,

- collect receivables aggressively,

- manage inventory carefully,

- control spending deliberately,

- and maintain adequate reserves.

When cash consistently enters the business before obligations become due, management stays in control.

When obligations arrive before cash does, financial pressure begins to control the business.

For small businesses, cash flow is not just an accounting number.

It is the foundation of operational survival and sustainable growth of your business.